Goods and Services Tax (GST) |

|

The Goods and Services Tax (GST), the biggest reform in India's indirect tax structure rather we can say that the biggest business reform in India since Independence, at last set to become reality and which may be roll out from 1st July 2017.

|

|

|

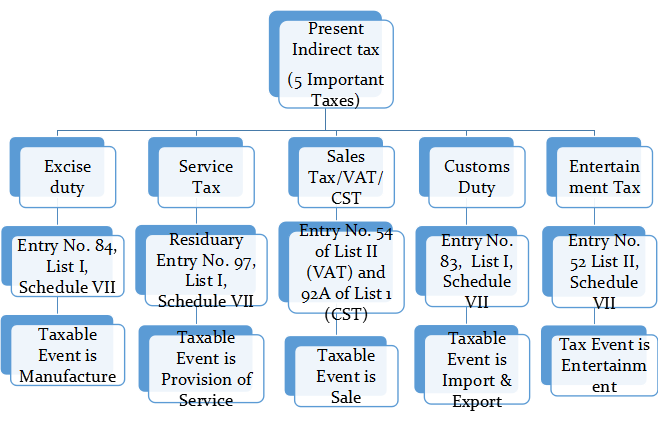

Presently, Central Government is empowered to levy excise duty on manufacturing and service tax on the supply of services. Further, State Governments has the power to levy sales tax or value added tax (VAT) on the sale of goods and various other taxes/duties as been empowered under the constitution.

|

|

|

In present scenario of Indirect Tax.

|

|

|

- There is no uniformity of tax rates and structure across States.

- There is cascading of taxes due to 'tax on tax'.

- No credit of excise duty and service tax paid at the stage of manufacture/supply of services are available to the traders while paying the State level sales tax or VAT, and vice-versa.

- Further, no credit of State taxes paid in one State can be availed in other States.

Hence, the prices of goods and services get artificially inflated to the extent of this 'tax on tax'.

|

| |

GST

|

Dual GST: Both Centre and States will simultaneously levy GST across the value chain on the same base. Tax will be levied on every supply of goods and services.

- CGST: Centre would levy and collect Central Goods and Services Tax (CGST) on intra state supply.

- SGST: States would levy and collect the State Goods and Services Tax (SGST) on all transactions within a State.

- IGST: The Centre would levy and collect the Integrated Goods and Services Tax (IGST) on all inter-State supply of goods and services and apportioned with the concerned state.

|

|

|

Under GST following Central and states Taxes will be subsumed:

|

|

| Central Taxes |

State Taxes |

| Central Sales Tax |

State VAT / Sales Tax |

| Central Excise duty (CENVAT) |

Purchase Tax |

| Additional Duties of Excise |

Entertainment Tax |

| Additional Duties of Customs (CVD & SAD) |

Luxury Tax |

| Service Tax |

Entry Tax ( All forms) |

| Surcharges & Cess |

Taxes on lottery, betting & gambling |

|

Surcharges & Cess |

|

What is excluded from GST

- Petroleum crude;

- High speed diesel;

- Motor spirit (commonly known as petrol);

- Natural gas;

- Aviation turbine fuel; and

- Alcohol for Human Consumption;

- Electricity Duty;

|

Benefits to Assesse

- Single Tax to replace Multiple Levies.

- Single Tax Liveable on Goods & Services

- Mitigation of cascading/ double taxation.

- More efficient neutralization of taxes especially for exports.

- Simpler tax regime -

- Fewer rates and exemptions.

- Conceptual clarity (Goods vs. Services).

|

KEY FEATURES OF THE GST

|

| 1. Persons who are liable to registered: If the aggregate turnover in a financial year exceeds Rs. 19 lakhs, it is supplier's duty to get registered under this law. The cap for suppliers in the Northeastern and hill states is Rs. 9 lakhs. The person who is required to be registered will be considered as taxable person under this law and is liable to pay tax if his aggregate turnover in a financial year exceeds Rs. 20 lakhs |

|

| Some categories of persons who shall be required to be registered under this Act irrespective of the threshold like persons making interstate supply, persons required to pay tax under reverse charge, nonresident taxable persons. Etc. |

|

| 2. Place of registration: The place of registration should be from where the goods or services are supplied. This helps with virtual marketplaces, mainly e-commerce. For each state the taxable person will have to take separate registration even though the taxable person supplying the goods/services or both from more than one state as single entity. |

|

| 3. Migration of existing taxpayers from GST: Every person already registered under the existing law will be issued a provisional certificate of registration. This certificate shall be valid for a period of six months, hence giving them enough time to make the changes in their model and furnish the required information, before the final certificate is provided. |

|

| 4. Taxable Event: Supply activities of goods or services such as sale, transfer, barter, exchange, license, rental, lease or disposal made or agreed to be made for consideration are all taxable events. Importation of services, whether or not for consideration or supply specified in schedule I, made or agreed to be made without a consideration are all taxable events. |

|

5. Point of taxation for supply of goods at the earliest of the following dates:

- Date on which the goods are removed for supply to the recipient (in the case of movable goods).or

- Date on which the goods are made available to the recipient (in the case of immovable goods).

- Date of issuing invoice by supplier.

- Date of receipt of payment by supplier.

- Date on which recipient shows the receipt of the goods in his books of account.

|

|

6. Point of taxation for supply of services shall be:-

- If the invoice is issued within the prescribed period: - The date of issue of invoice or the date of receipt of payment, whichever is earlier

- If the invoice is not issued within the prescribed period:- The date of completion of the provision of services or the date of receipt of payment whichever is earlier.

- The date on which the recipient shows the receipt of the services in his books of account, in case where the above provisions do not apply.

|

|

| 7. Determination of Valuation: The value of a supply of goods or services shall normally be the transaction value. In case, the valuation cannot be determined by the transaction or supply value, the valuation can be made by supply or transaction value of similar products and services. {As per GST valuation (Determination of the value of Supply of goods and services) Rules, 2016)} |

|

| 8. Utilization of credit: Every registered taxable person shall be entitled to take credit of admissible input tax. The input tax credit is credited to the electronic credit ledger. |

|

| In the case of excess of credit in any of the three taxes in question, it can be utilized as under:- |

|

| Input tax |

Output tax |

| CGST |

1st Preference: CGST

2nd preference: IGST

|

| SGST |

1st Preference: SGST

2nd preference: IGST

|

| IGST |

1st Preference: IGST

2nd preference: CGST

3rd Preference : SGST

|

|

|

| 9. Returns: The following returns must be filed by all the suppliers:- |

|

| S.No. |

Form No. |

Purpose |

Due Date |

| 1 |

GSTR-1 |

Outward supplies made by supplier |

10th of next month |

| 2 |

GSTR-2 |

Inward supplies received by a tax payer |

15th of next month |

| 3 |

GSTR-3 |

Monthly return |

20th of next month |

| 4 |

GSTR-4 |

Quarterly return for compounding Tax payer |

18th of next month |

| 5 |

GSTR-5 |

Periodic return by non -resident foreign tax payer |

Last day of registration |

| 6 |

GSTR-6 |

Return for Input Service Distributor |

13th of next month |

| 7 |

GSTR-7 |

Return for Tax Deducted at source |

10th of next month |

| 8 |

GSTR-8 |

Return for Tax Collection at source |

10th of next month |

| 9 |

GSTR-9 |

Annual Return |

31st Dec of next yeaR |

|

|